The One Thing Every Homeowner Needs To Know About a Recession

The One Thing Every Homeowner Needs To Know About a Recession

A recession does not equal a housing crisis. That’s the one thing that every homeowner today needs to know. Everywhere you look, experts are warning we could be heading toward a recession, and if true, an economic slowdown doesn’t mean homes will lose value.

The National Bureau of Economic Research (NBER) defines a recession this way:

“A recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators. A recession begins when the economy reaches a peak of economic activity and ends when the economy reaches its trough. Between trough and peak, the economy is in an expansion.”

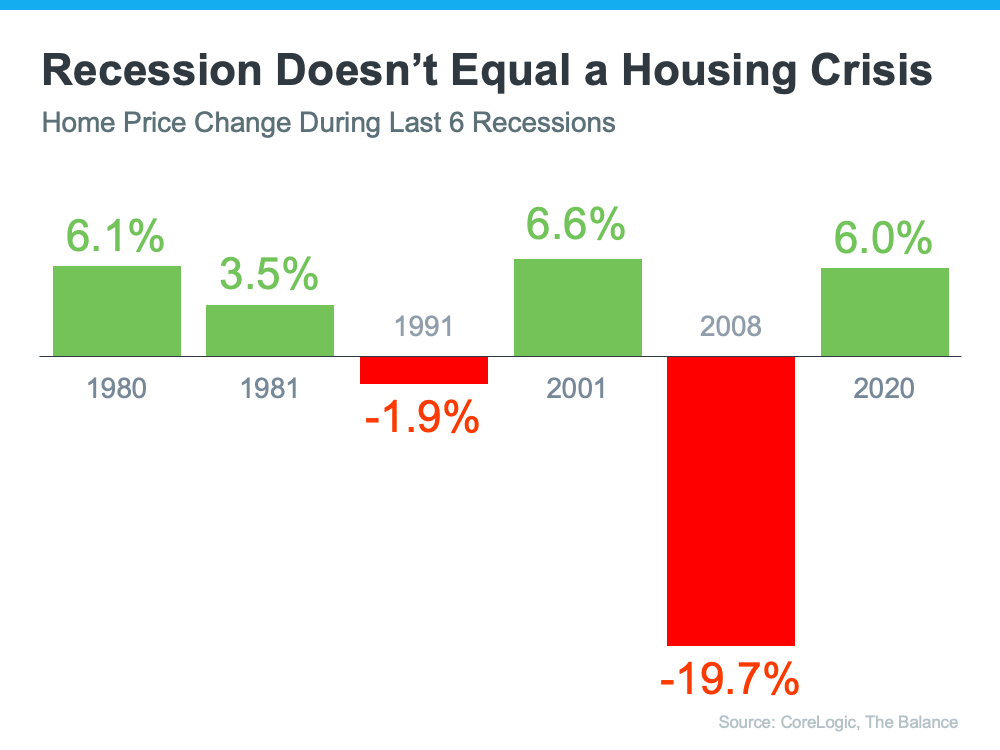

To help show that home prices don’t fall every time there’s a recession, take a look at the historical data. There have been six recessions in this country over the past four decades. As the graph below shows, looking at the recessions going all the way back to the 1980s, home prices appreciated four times and depreciated only two times. So, historically, there’s proof that when the economy slows down, it doesn’t mean home values will fall or depreciate.

The first occasion on the graph when home values depreciated was in the early 1990s when home prices dropped by less than 2%. It happened again during the housing crisis in 2008 when home values declined by almost 20%. Most people vividly remember the housing crisis in 2008 and think if we were to fall into a recession that we’d repeat what happened then. But this housing market isn’t a bubble that’s about to burst. The fundamentals are very different today than they were in 2008. So, we shouldn’t assume we’re heading down the same path.

Bottom Line

We’re not in a recession in this country, but if one is coming, it doesn’t mean homes will lose value. History proves a recession doesn’t equal a housing crisis.

Marty Gale

Buy or Sell with Marty Gale

"Its The Experience"

Principal Broker and Owner of Utah Realty™

Licensed Since 1986

CERTIFIED LUXURY HOME MARKETING SPECIALIST (CLHM)

PSA (Pricing Strategy Advisor)

General Contractor 2000 (in-active)

e-pro (advanced digital marketing) 2001

Certified Residential Specialist 2009

Certified Negotiation Expert 2014

Master Certified Negotiation Expert 2014

Certified Probate Specialist Since 2018

Senior Real Estate Specialist

Certified Divorce Specialist CDS

![]()

Contact me!

How Homeownership Can Bring You Joy

How Homeownership Can Bring You Joy

If you’re trying to decide whether to rent or buy a home, you’re probably weighing a few different factors. The financial benefits of homeownership might be one of the reasons you want to make a purchase if you’re a renter, but the decision can also be motivated by having a place that’s uniquely your own.

If you want to express yourself by upgrading and customizing your living space but are feeling held back by your rental agreement, it might be time to consider the perks of owning your home.

A Little Change Can Bring Lots of Joy

There’s a significant level of pride that comes from owning a home. That’s because it’s a space that truly belongs to you.

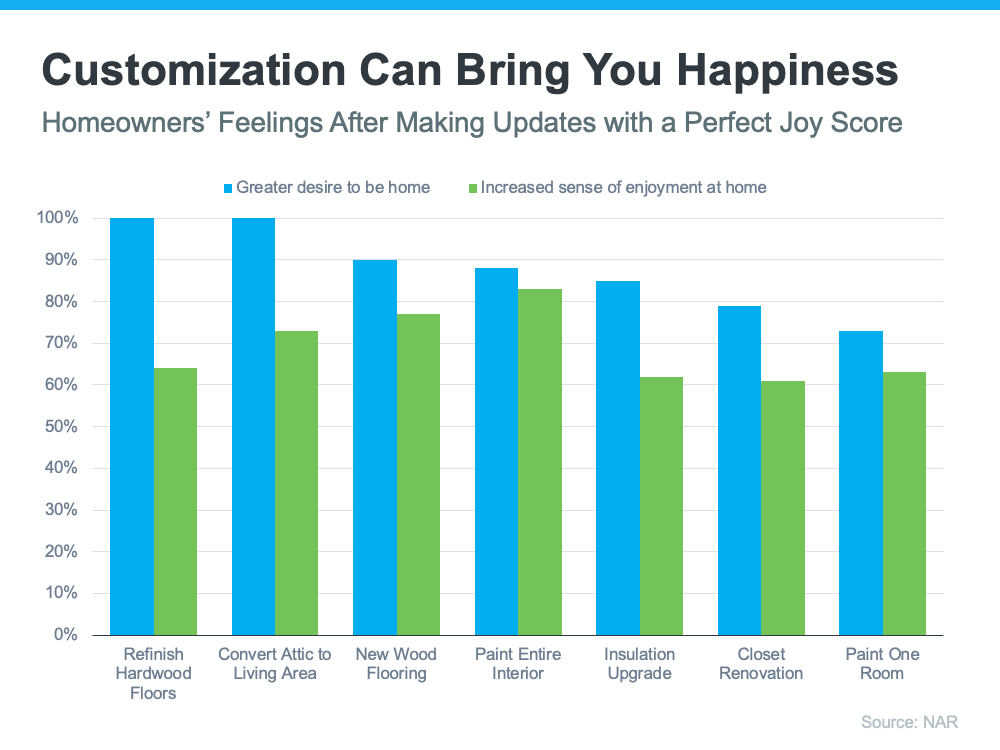

A recent report from the National Association of Realtors (NAR) shows making updates or remodeling your home can help you feel more at ease and comfortable in your living space. NAR measures this with a Joy Score that indicates how much happiness specific home upgrades bring. According to NAR:

“There were numerous interior projects that received a perfect Joy Score of 10: paint entire interior of home, paint one room of home, add a new home office, hardwood flooring refinish, new wood flooring, closet renovation, insulation upgrade, and attic conversion to living area.”

The report also breaks down just how much each of these projects can enhance your emotional attachment to your home, even leading you to want to spend even more time in the space (see graph below):

And while many of the items NAR highlights are larger tasks, some, like painting rooms, are much smaller. Even those quicker projects can still bring you a greater sense of joy and accomplishment. Not to mention when you make upgrades in your home, you could be increasing its value which also gives your net worth a boost if you invest your time and effort wisely.

You’re Free To Update Your Home to Your Heart’s Content

These types of updates can result in additional happiness when you complete them, but there’s another reason you can feel good as a homeowner. In most situations, you’re free to renovate or update the interior of your home without needing additional permission. But as Business Insider points out, renters may not have the same freedom:

“Your landlord won’t always approve changes when you rent. But you have the power to update the home when you’re the owner. (Just make sure any big changes are approved by your homeowner’s association, if necessary.)”

If you do make changes as a renter, there’s a good chance you’ll need to revert them back at the end of your lease based on your rental agreement. That can add additional costs when you move out. That’s one major benefit of owning your own home. Unless there are specific homeowner’s association requirements, you typically won’t have to worry about the changes you can and can’t make.

Bottom Line

Deciding whether to rent or buy is a personal decision. The financial benefits are critical, but don’t overlook the emotional impact homeownership can have. Let’s connect to discuss all the benefits you can enjoy when you purchase your own home.

Should You Update Your House Before Selling? Ask a Real Estate Professional.

Should You Update Your House Before Selling? Ask a Real Estate Professional.

Some Highlights

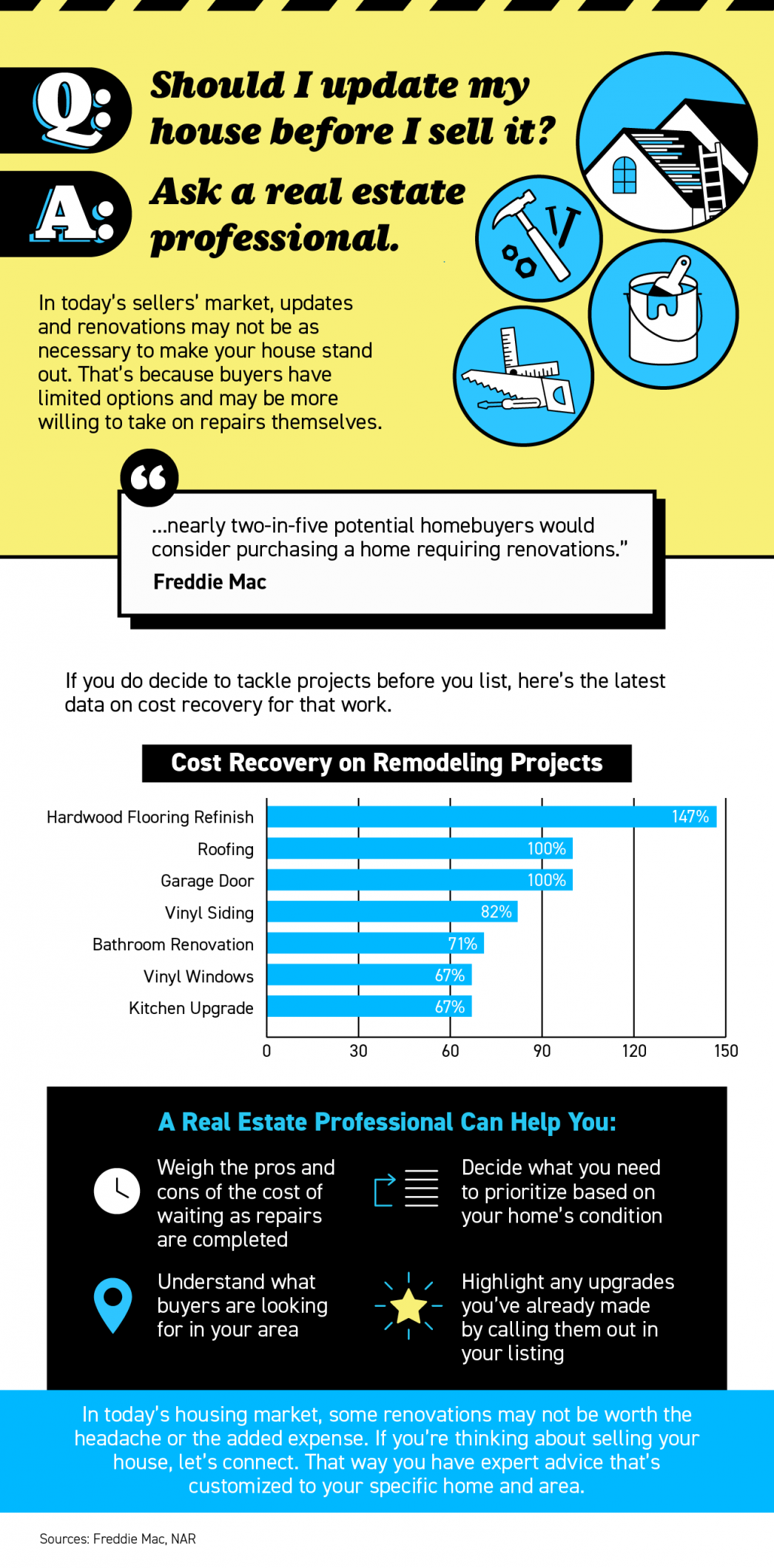

- If you’re deciding whether you should make updates before you sell your house, lean on your trusted real estate advisor to be your guide.

- In today’s sellers’ market, buyers have limited options and may be more willing to take on repairs themselves.

- If you’re thinking about selling your house, let’s connect so you have expert advice that’s customized to your home and our local area.

Marty Gale

Buy or Sell with Marty Gale

"Its The Experience"

Principal Broker and Owner of Utah Realty™

Licensed Since 1986

CERTIFIED LUXURY HOME MARKETING SPECIALIST (CLHM)

PSA (Pricing Strategy Advisor)

General Contractor 2000 (in-active)

e-pro (advanced digital marketing) 2001

Certified Residential Specialist 2009

Certified Negotiation Expert 2014

Master Certified Negotiation Expert 2014

Certified Probate Specialist Since 2018

Senior Real Estate Specialist

Certified Divorce Specialist CDS

![]()

Contact me!

Top Signs It’s Time To Sell According to Experts

What You Actually Need To Know About the Number of Foreclosures in Today’s Housing Market

What You Actually Need To Know About the Number of Foreclosures in Today’s Housing Market

While you may have seen recent stories about the volume of foreclosures today, context is important. During the pandemic, many homeowners were able to pause their mortgage payments using the forbearance program. The goal was to help homeowners financially during the uncertainty created by the health crisis.

When the forbearance program began, many experts were concerned it would result in a wave of foreclosures coming to the market, as there was after the housing crash in 2008. Here’s a look at why the number of foreclosures we’re seeing today is nothing like the last time.

1. There Are Fewer Homeowners in Trouble

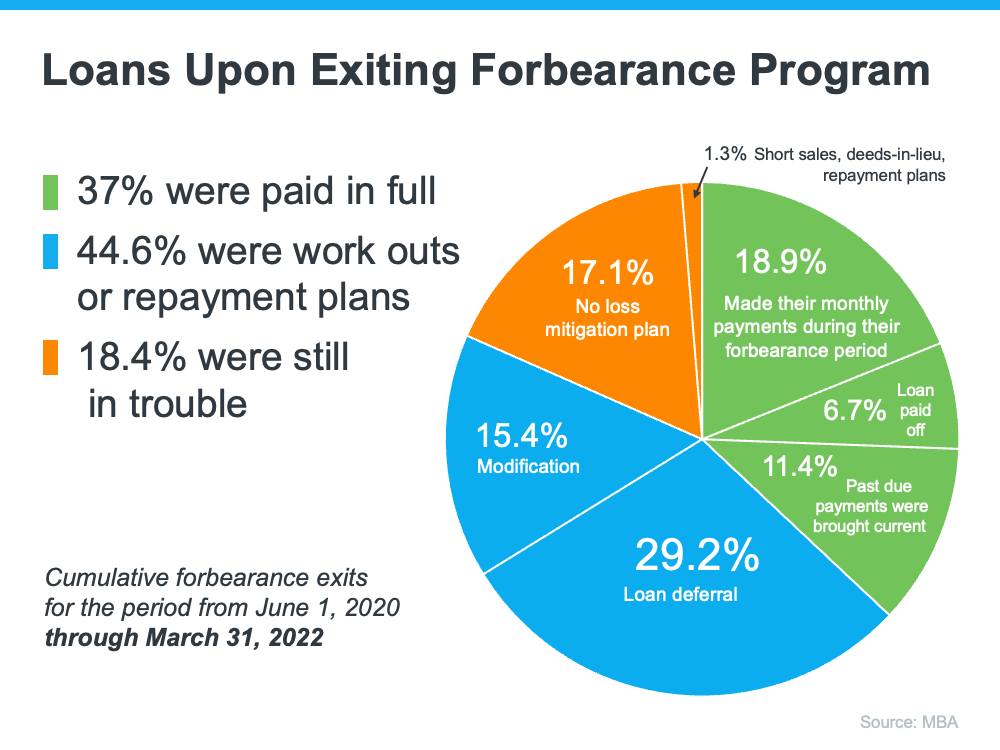

Today’s data shows that most homeowners are exiting their forbearance plan either fully caught up on payments or with a plan from the bank that restructured their loan in a way that allowed them to start making payments again. The graph below depicts those findings from the Mortgage Bankers Association (MBA):

The same MBA report mentioned above estimates there are approximately 525,000 homeowners who remain in forbearance today. Thankfully, those people still have the chance to work out a suitable repayment plan with the servicing company that represents their lender.

2. Most Homeowners Have Enough Equity To Sell Their Homes

For those who are exiting the forbearance program without a plan in place, many will have enough equity to sell their homes instead of facing foreclosures. Due to rapidly rising home prices over the last two years, the average homeowner has gained record amounts of equity in their home.

Marina Walsh, CMB, Vice President of Industry Analysis at MBA, says:

“Given the nation’s limited housing inventory and the variety of home retention and foreclosure alternatives on the table across various loan types, . . . Borrowers have more choices today to either stay in their homes or sell without resorting to a foreclosure.”

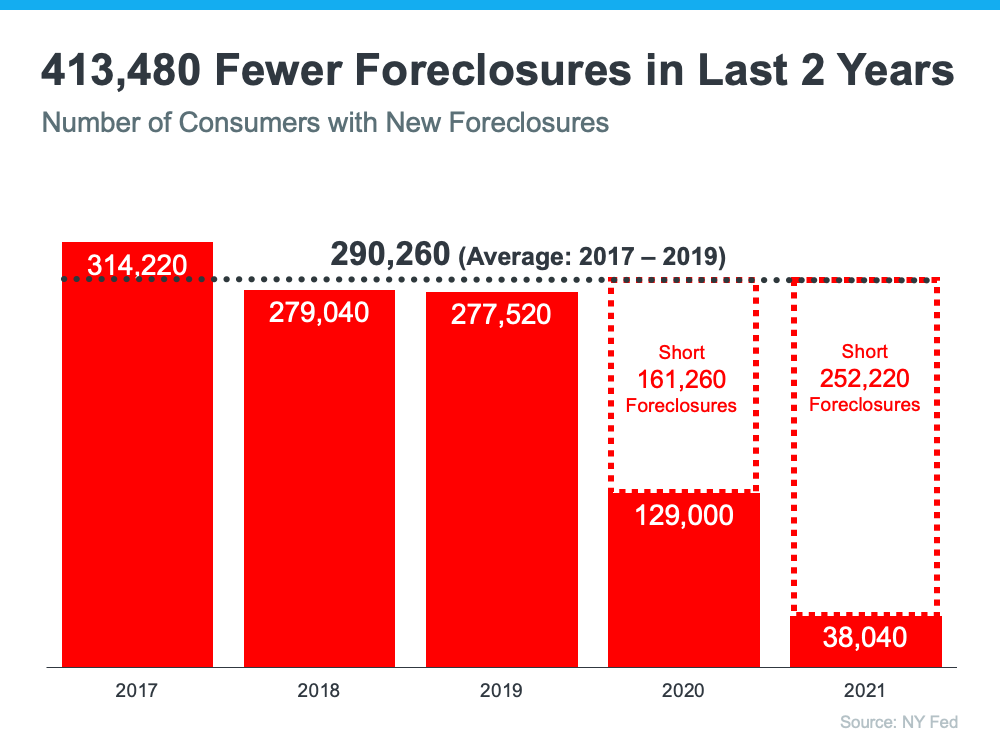

3. There Have Been Fewer Foreclosures over the Last Two Years

One of the seldom-reported benefits of the forbearance program was it gave homeowners facing difficulties an extra two years to get their finances in order and work out a plan with their lender. That helped prevent the foreclosures that normally would have come to the market had the new forbearance program not been available.

Even as people leave the forbearance program, there are still fewer foreclosures happening today than before the pandemic. That means, while there are more foreclosures now compared to last year (when foreclosures were paused), the number is still well below what the housing market has seen in a more typical year, like 2017-2019 (see graph below):

4. The Current Market Can Easily Absorb New Listings

When the foreclosures in 2008 hit the market, they added to the oversupply of houses that were already for sale. It’s exactly the opposite today. The latest Existing Home Sales Report from the National Association of Realtors (NAR) reveals:

“Total housing inventory at the end of March totaled 950,000 units, up 11.8% from February and down 9.5% from one year ago (1.05 million). Unsold inventory sits at a 2.0-month supply at the present sales pace, up from 1.7 months in February and down from 2.1 months in March 2021.”

A balanced market would have approximately a six-month supply of inventory. At 2.0 months, today’s housing market is severely understocked. Even if one million homes enter the market, there still won’t be enough inventory to meet the current demand.

Bottom Line

If you see headlines about the increasing number of foreclosures today, remember context is important. While it’s true the number of foreclosures is higher now than it was last year, foreclosures are still well below pre-pandemic years.

If you have questions, let’s connect to talk through the latest market conditions and what they mean for you.

Are There More Homes Coming to the Market?

Are There More Homes Coming to the Market?

According to a recent survey from the National Association of Realtors (NAR), one of the top challenges buyers face in today’s housing market is finding a home that meets their needs. That’s largely because the inventory of homes for sale is so low today.

If you’re looking to buy a home, you may have noticed this yourself. But there is good news. Recent data shows more sellers are listing their houses this season, which may give you more options for your home search.

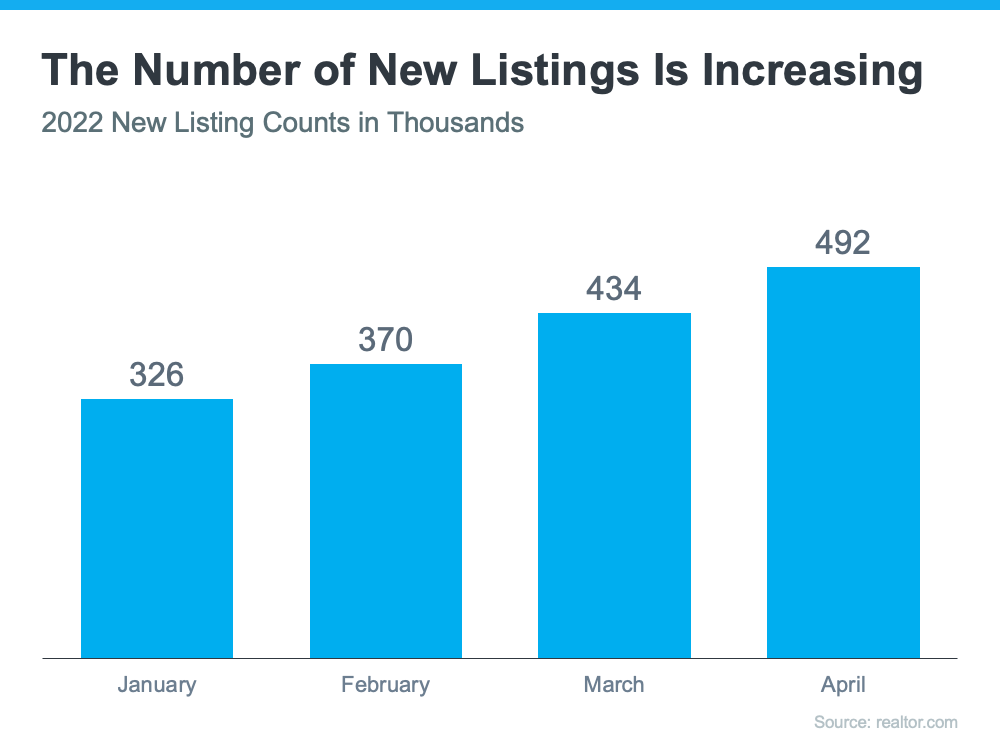

Early Signs Inventory May Be Growing

The latest data from realtor.com shows the number of listings coming onto the market, known in the industry as “new listings,” has increased since the start of the year (see graph below):

This indicates more sellers are listing their homes for sale each month this year. And according to realtor.com, this growth is expected to continue. Their research finds the majority of potential sellers plan to list their homes over the next six months. Realtor.com says:

“. . . markets may see a noticeable bump in the number of homes for sale as we move through spring and into summer. A majority of homeowners planning to sell this year indicated that they aim to list in the next six months, with almost 10% having already placed their properties on the market.”

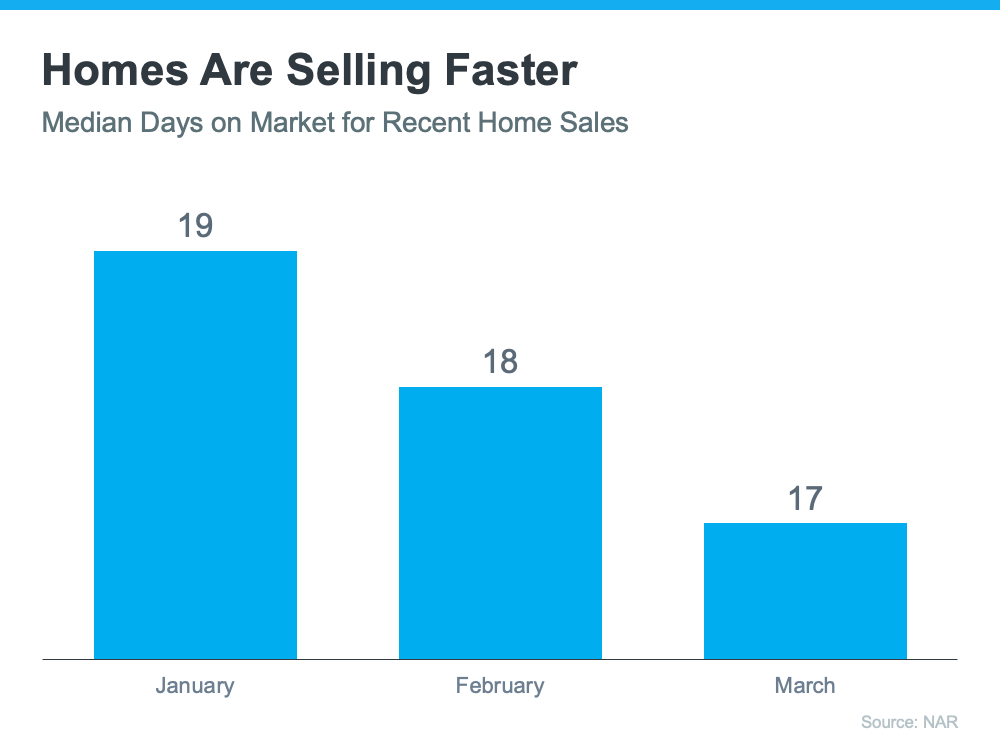

Homes Are Still Selling Quickly

But while new listings are increasing, it’s important to know they’re also selling quickly. The latest Realtors Confidence Index from NAR shows the median days on market for recently sold homes since the beginning of the year (see chart below). The time on market has decreased month-over-month. That means homes are selling even faster than they did the previous month.

What That Means for You

While a low-inventory market is difficult to navigate as a buyer, there is hope. The growing number of new listings and the expectation more sellers will list their homes in the coming months is great news if you’ve had a hard time finding a home that fits your needs. Just remember, those new listings are going fast. That means you’ll want to keep your foot on the gas and be ready to act if you find a home you love this season.

Your agent can help you stay on top of the latest listings in your area so you can find the home that’s right for you and submit your strongest offer as quickly as possible.

Bottom Line

If you’ve been having a hard time finding your dream home, stick with your search. More options are coming to market and your ideal home could be one of them. Let’s connect so you can stay up to date on the latest listings in our market, so you can be ready to move fast when you find the one that’s right for you.

Will Home Prices Fall This Year? Here’s What Experts Say

Will Home Prices Fall This Year? Here’s What Experts Say.

Many people are wondering: will home prices fall this year? Whether you’re a potential homebuyer, seller, or both, the answer to this question matters for you. Let’s break down what’s happening with home prices, where experts say they’re headed, and how this impacts your homeownership goals.

What’s Happening with Home Prices?

Home prices have seen 121 consecutive months of year-over-year increases. CoreLogic says:

“Price appreciation averaged 15% for the full year of 2021, up from the 2020 full year average of 6%.”

So why are prices climbing so much? It’s because there are more buyers than there are homes for sale. This imbalance is expected to maintain that upward pressure on home prices because homes for sale are a hot commodity in today’s low-inventory housing market.

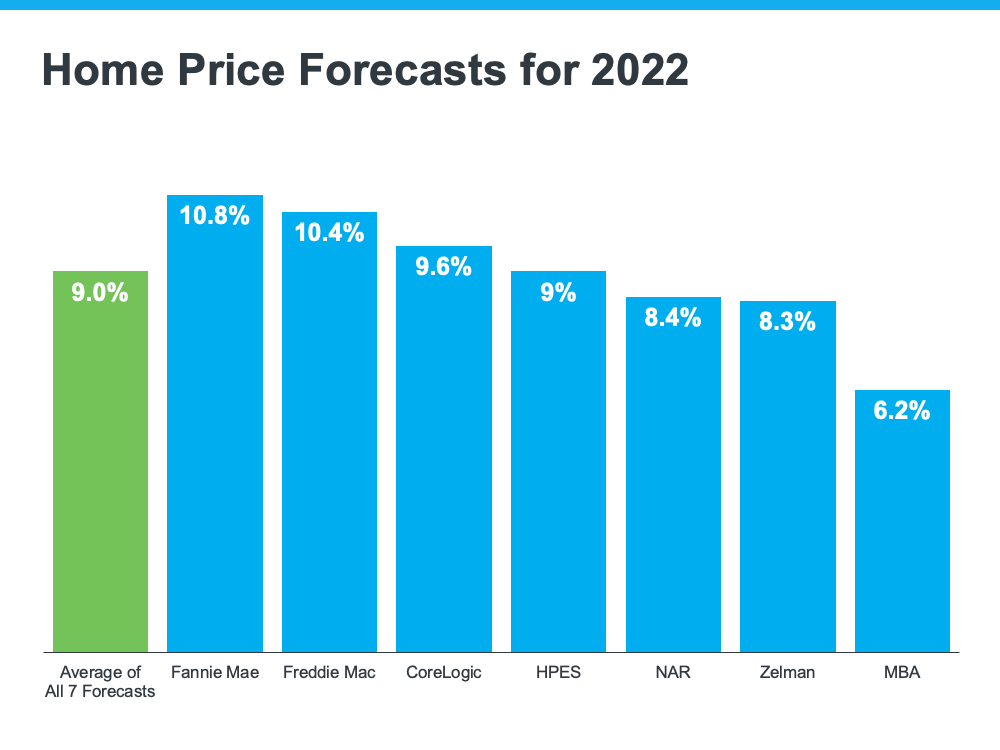

Where Do Experts Say Prices Will Go from Here?

Experts say the housing market isn’t set up for a price decline due to that ongoing imbalance between supply and demand. In the latest home price forecasts for 2022, they’re calling for ongoing appreciation throughout the year (see graph below):

While the experts are forecasting more moderate price appreciation, the 2022 projections show price gains will remain strong throughout this year. First American explains it like this:

“While house price growth is expected to moderate from the rapid pace of 2021, strong home buyer demand against a backdrop of historically tight inventory of homes for sale will likely keep appreciation positive in the coming year.”

What Does That Mean for You?

The biggest takeaway is that none of the experts are projecting depreciation. If you’re a homeowner thinking about selling, the higher price appreciation over the last two years has been great for your home’s value, but it’s also something you should factor in when planning your next steps. If you’ll also be buying a home after selling your current house, you shouldn’t wait for prices to fall. Waiting will only cost you more in the long run because climbing mortgage rates and rising home prices will have an impact on your next home purchase. Freddie Mac says:

“If you’re thinking about waiting until next year and that maybe rates are higher, but you’ll get a deal on prices – well that’s risky. It may be more advantageous to purchase this year relative to waiting until 2023 at this time.”

Bottom Line

If you’re thinking of selling to move up, you shouldn’t wait for prices to fall. Experts say prices will continue to appreciate this year. That means, if you’re ready, buying your next home before prices climb further may make the most financial sense. Let’s connect to begin the process of selling your current home and looking for your next one before prices rise higher.

The Dream of Homeownership Is Worth the Effort

The Dream of Homeownership Is Worth the Effort

If you’re in the market to buy a home this season, stick with it. Homebuyers face challenges in any market, and today’s is no exception. But if you persevere, your decision to purchase a home will be worth the effort in the end. In fact, a recent survey from Bankrate shows homeownership is so powerful that:

“Nearly three in four homeowners say they would still buy their current home if they had it to do [sic] all over again.”

That means the results – owning a home and the benefits that come with it – outweigh the effort needed to achieve their goal. If you’re a homebuyer, let that provide you with the confidence to know the work you’re putting in today will pay off for years to come. Here are a few reasons to stick with your search and focus on the outcome.

Homeownership Contributes Significantly to Your Financial Well-Being

The National Association of Realtors (NAR) lists several motivations to consider if you’re thinking about buying a home. One of the top financial reasons is the equity you build. As NAR says:

“Money paid for rent is money that you’ll never see again, but mortgage payments let you build equity . . . Building equity in your home is a ready-made savings plan.”

Your equity is a powerful tool you can leverage in a number of ways. And with recent home price appreciation, homeowners are seeing record levels of equity today. That may be one reason why so many people view owning a home as a great investment and a top indicator of financial well-being. As the survey from Bankrate mentioned above shows:

“. . . Americans place a higher value on homeownership than on any other indicator of economic stability, . . .”

Owning a home ranks above other major accomplishments like retirement, having a successful career, and getting a college degree. That indicates just how impactful the financial benefits of homeownership truly are.

The Emotional Benefits of Owning a Home Are Powerful

Of course, homeownership is more than an investment. In their list of top reasons to buy a home, NAR also highlights some of the powerful, non-financial aspects of homeownership. Among them is the opportunity to customize your home to reflect your personality and needs. As they say:

“The home is yours. You can decorate any way you want and choose the types of upgrades and new amenities that appeal to your lifestyle.”

Another benefit homeowners enjoy is the stability it provides. Homeowners typically stay put longer than renters. According to NAR, when you remain in one place longer than a few years, you can grow closer to your community. And that can enhance your sense of pride and lead to better relationships.

What Does That Mean for You?

The benefits of homeownership are powerful, as Leslie Rouda Smith, President of NAR, says:

“From building personal wealth and fostering communities, to strengthening social stability and driving the national economy, the value of homeownership is indisputable.”

Even if you face challenges in today’s market, the payoff when you succeed and purchase a home will be worth it.

Bottom Line

If you’re planning to buy a home this year, there are incredible benefits waiting for you at the end of your journey. Let’s connect to discuss everything homeownership has to offer.

How Homeownership Can Help Shield You from Inflation

How Homeownership Can Help Shield You from Inflation

If you’re following along with the news today, you’ve likely heard about rising inflation. You’re also likely feeling the impact in your day-to-day life as prices go up for gas, groceries, and more. These rising consumer costs can put a pinch on your wallet and make you re-evaluate any big purchases you have planned to ensure they’re still worthwhile.

If you’ve been thinking about purchasing a home this year, you’re probably wondering if you should continue down that path or if it makes more sense to wait. While the answer depends on your situation, here’s how homeownership can help you combat the rising costs that come with inflation.

Homeownership Offers Stability and Security

Investopedia explains that during a period of high inflation, prices rise across the board. That’s true for things like food, entertainment, and other goods and services, even housing. Both rental prices and home prices are on the rise. So, as a buyer, how can you protect yourself from increasing costs? The answer lies in homeownership.

Buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. If you get a fixed-rate mortgage on your home, you lock in your monthly payment for the duration of your loan, often 15 to 30 years. James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

So even if other prices rise, your housing payment will be a reliable amount that can help keep your budget in check. If you rent, you don’t have that same benefit, and you won’t be protected from rising housing costs.

Use Home Price Appreciation to Your Benefit

While it’s true rising mortgage rates and home prices mean buying a house today costs more than it did a year ago, you still have an opportunity to set yourself up for a long-term win. Buying now lets you lock in at today’s rates and prices before both climb higher.

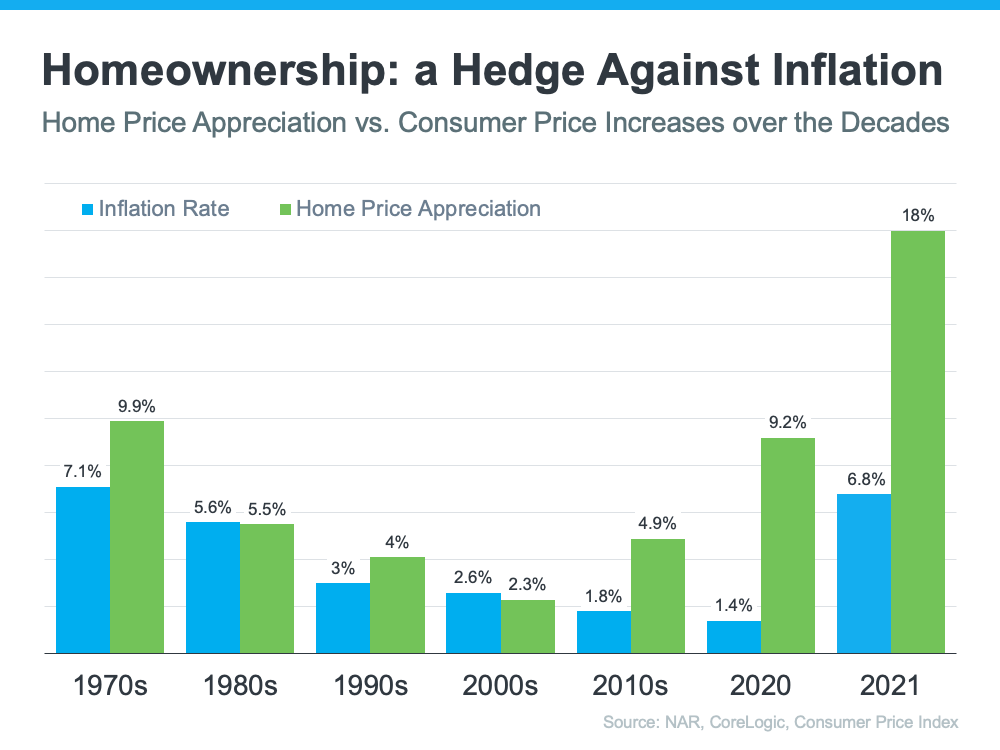

In inflationary times, it’s especially important to invest your money in an asset that traditionally holds or grows in value. The graph below shows how home price appreciation outperformed inflation in most decades going all the way back to the seventies – making homeownership a historically strong hedge against inflation (see graph below):

So, what does that mean for you? Today, experts say home prices will only go up from here thanks to the ongoing imbalance in supply and demand. Once you buy a house, any home price appreciation that does occur will be good for your equity and your net worth. And since homes are typically assets that grow in value (even in inflationary times), you have peace of mind that history shows your investment is a strong one.

Bottom Line

If you’re ready to buy a home, it may make sense to move forward with your plans despite rising inflation. If you want expert advice on your specific situation and how to time your purchase, let’s connect.

If you’re following along with the news today, you’ve likely heard about rising inflation. You’re also likely feeling the impact in your day-to-day life as prices go up for gas, groceries, and more. These rising consumer costs can put a pinch on your wallet and make you re-evaluate any big purchases you have planned to ensure they’re still worthwhile.

If you’ve been thinking about purchasing a home this year, you’re probably wondering if you should continue down that path or if it makes more sense to wait. While the answer depends on your situation, here’s how homeownership can help you combat the rising costs that come with inflation.

Homeownership Offers Stability and Security

Investopedia explains that during a period of high inflation, prices rise across the board. That’s true for things like food, entertainment, and other goods and services, even housing. Both rental prices and home prices are on the rise. So, as a buyer, how can you protect yourself from increasing costs? The answer lies in homeownership.

Buying a home allows you to stabilize what’s typically your biggest monthly expense: your housing cost. If you get a fixed-rate mortgage on your home, you lock in your monthly payment for the duration of your loan, often 15 to 30 years. James Royal, Senior Wealth Management Reporter at Bankrate, says:

“A fixed-rate mortgage allows you to maintain the biggest portion of housing expenses at the same payment. Sure, property taxes will rise and other expenses may creep up, but your monthly housing payment remains the same.”

So even if other prices rise, your housing payment will be a reliable amount that can help keep your budget in check. If you rent, you don’t have that same benefit, and you won’t be protected from rising housing costs.

Use Home Price Appreciation to Your Benefit

While it’s true rising mortgage rates and home prices mean buying a house today costs more than it did a year ago, you still have an opportunity to set yourself up for a long-term win. Buying now lets you lock in at today’s rates and prices before both climb higher.

In inflationary times, it’s especially important to invest your money in an asset that traditionally holds or grows in value. The graph below shows how home price appreciation outperformed inflation in most decades going all the way back to the seventies – making homeownership a historically strong hedge against inflation (see graph below):

So, what does that mean for you? Today, experts say home prices will only go up from here thanks to the ongoing imbalance in supply and demand. Once you buy a house, any home price appreciation that does occur will be good for your equity and your net worth. And since homes are typically assets that grow in value (even in inflationary times), you have peace of mind that history shows your investment is a strong one.

Bottom Line

If you’re ready to buy a home, it may make sense to move forward with your plans despite rising inflation. If you want expert advice on your specific situation and how to time your purchase, let’s connect.

Marty Gale

Buy or Sell with Marty Gale

"Its The Experience"

Principal Broker and Owner of Utah Realty™

Licensed Since 1986

CERTIFIED LUXURY HOME MARKETING SPECIALIST (CLHM)

PSA (Pricing Strategy Advisor)

General Contractor 2000 (in-active)

e-pro (advanced digital marketing) 2001

Certified Residential Specialist 2009

Certified Negotiation Expert 2014

Master Certified Negotiation Expert 2014

Certified Probate Specialist Since 2018

Senior Real Estate Specialist

Certified Divorce Specialist CDS

![]()

Contact me!