when one door closes

As you set out to buy a home, saving for a down payment is likely top of mind. But you may still have questions about the process, including how much to save and where to start.

If that sounds like you, your down payment could be more in reach than you originally thought. Here’s why.

If you believe you have to put 20% down on a home, you may have based your goal on a common misconception. Freddie Mac explains:

“. . . nearly a third of prospective homebuyers think they need a down payment of 20% or more to buy a home. This myth remains one of the largest perceived barriers to achieving homeownership.”

Unless it’s specified by your loan type or lender, it’s typically not required to put 20% down. According to the latest Profile of Home Buyers and Sellers from the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. There are even loan types, like FHA loans, with down payments as low as 3.5%, as well as options like VA loans and USDA loans with no down payment requirements for qualified applicants.

This is good news for you because it means you could be closer to your homebuying dream than you realize. For more information, turn to a trusted lender.

A professional will be able to show you other options that could help you get closer to your down payment goal. According to latest Homeownership Program Index from downpaymentresource.com, there are over 2,000 homebuyer assistance programs in the U.S., and the majority are intended to help with down payments.

A recent article explains why programs like these are helpful:

“These resources can immediately build your home buying power and help you take action sooner than you thought possible.”

And if you’re wondering if you have to be a first-time buyer to qualify for these programs, that’s not always the case. According to an article from downpaymentresource.com:

“It is a common misconception that homebuyer assistance is only available to first-time homebuyers, however, 38% of homebuyer assistance programs in Q1 2022 did not have a first-time homebuyer requirement.”

There are also location and profession-based programs you could qualify for as well.

Saving for your down payment is an important first step on your homebuying journey. Let’s connect today and make sure you have a trusted lender to help explore your options.

![]()

![]()

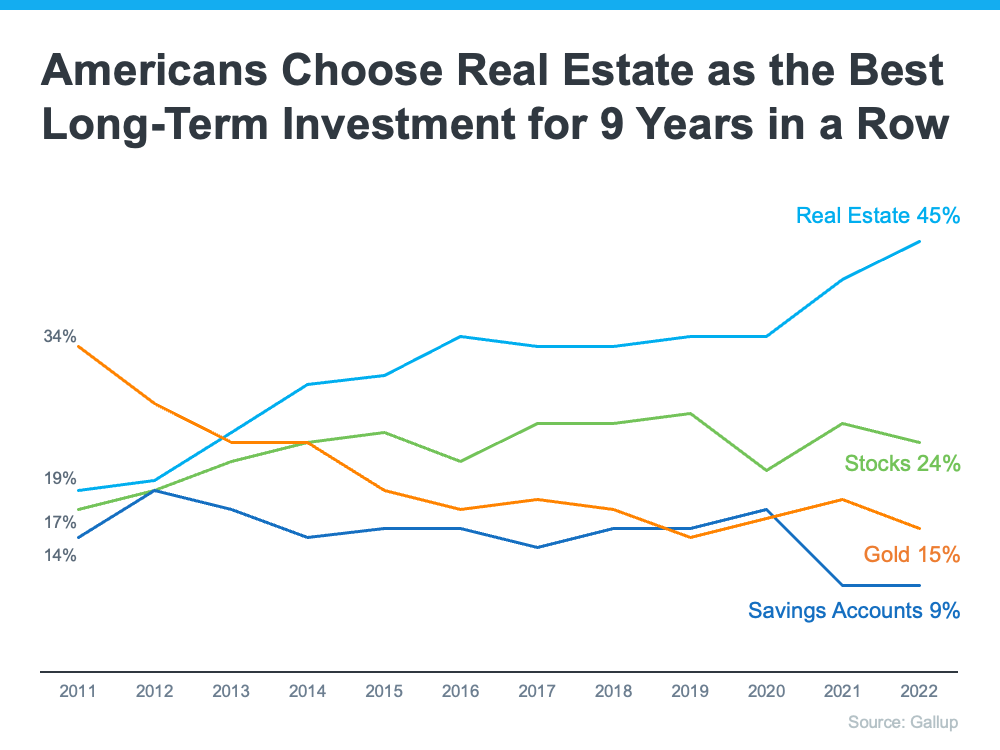

Americans’ opinion on the value of real estate as an investment is climbing. That’s according to an annual survey from Gallup. Not only is real estate viewed as the best investment for the ninth year in a row, but more Americans selected it than ever before.

The graph below shows the results of the survey since Gallup began asking the question in 2011. As the trend lines indicate, real estate has been gaining ground as the clear favorite for almost a decade now:

If you’re thinking about purchasing a home, let this poll reassure you. Even when inflation is high like today, Americans recognize owning a home is a powerful financial decision.

Because inflation reached its highest level in 40 years recently, it’s more important than ever to understand the financial benefits of homeownership. Rising inflation means prices are increasing across the board, and that includes goods, services, housing costs, and more. When you purchase your home, you lock in your monthly housing payments, effectively shielding yourself from increases on one of your biggest budgetary items each month.

If you’re a renter, you don’t have that same benefit, and you aren’t protected from these increases, especially as rents rise. As Danielle Hale, Chief Economist at realtor.com, notes:

“Rising rents, which continue to climb at double-digit pace . . . and the prospect of locking in a monthly housing cost in a market with widespread inflation are motivating today’s first-time homebuyers.”

Your house is also an asset that typically increases in value over time, even during inflation. That‘s because as prices rise, the value of your home does too. Mark Cussen, Financial Writer for Investopedia, puts it like this:

“There are many advantages to investing in real estate. . . . It often acts as a good inflation hedge since there will always be a demand for homes, regardless of the economic climate, and because as inflation rises, so do property values. . . .”

And since rising home values help increase your equity, and by extension your net worth, homeownership is historically a good hedge against inflation.

Buying a home is a powerful decision. It’s no wonder why so many people view it as the best long-term investment, even when inflation is high. When you buy, you help shield yourself from increases in your housing costs and you own an asset that typically gains value with time. If you want to better understand how buying a home could be a great investment for you, let’s connect today.

![]()

June is National Homeownership Month, and it’s the perfect time to reflect on how impactful owning a home can truly be. When you purchase a house, it becomes more than just a space you occupy. It’s your stake in the community, an investment, and a place you can put your stamp on.

If you’re thinking about buying a home this year, here are some of the benefits you’ll experience when you do.

Because it’s a place that’s uniquely yours, owning a home can give you a sense of pride and happiness in several ways.

Investopedia puts it like this:

“One often-cited benefit of homeownership is the knowledge that you own your little corner of the world.”

That knowledge can lead to a powerful, emotional connection to the place where you live. But so can the realization that your home will grow with you. Because it’s yours, you have the freedom to make updates to it as your needs and tastes change. As Logan Mohtashami, Lead Analyst for HousingWire, says:

“The psychology is that this is yours and you’re going to make it as good as possible because you’re in for a long time, . . . “

And that can create a greater sense of ownership, pride, and connection with your home and your community.

Homeownership can lead you to get even more involved with your local area. After all, you’re putting your roots down in a location and will want to do what you can to help improve it, much like your home. In a recent report, the National Association of Realtors (NAR) says:

“Living in one place for a longer amount of time creates and [sic] obvious sense of community pride, which may lead to more investment in said community.”

When you choose to become a homeowner, you’re making a financial decision as well. That’s because your home is also an investment.

Homeownership is truly one of the best ways to improve your long-term financial position. Not only will you have a predictable monthly housing expense that can benefit your budget in the short term, but you’ll also gain equity as your home appreciates in value and you make your monthly mortgage payment. As Freddie Mac says:

“Building equity through your monthly principal payments and appreciation is a critical part of homeownership that can help you create financial stability.”

Because of your growing equity, you can build your net worth as a homeowner. And when you compare the difference in net worth between a renter and a homeowner, it’s clear that owning a home truly offers a great way to build your long-term financial position.

According to the latest data from NAR, the median household net worth of a homeowner is roughly $300,000, while the median net worth of renters is only about $8,000. That means a homeowner’s net worth is nearly 40 times that of a renter.

Homeownership is truly a way to find greater satisfaction and happiness and to build financial freedom. If National Homeownership Month has you dreaming about purchasing a home, then let’s connect to begin the process today.

![]()

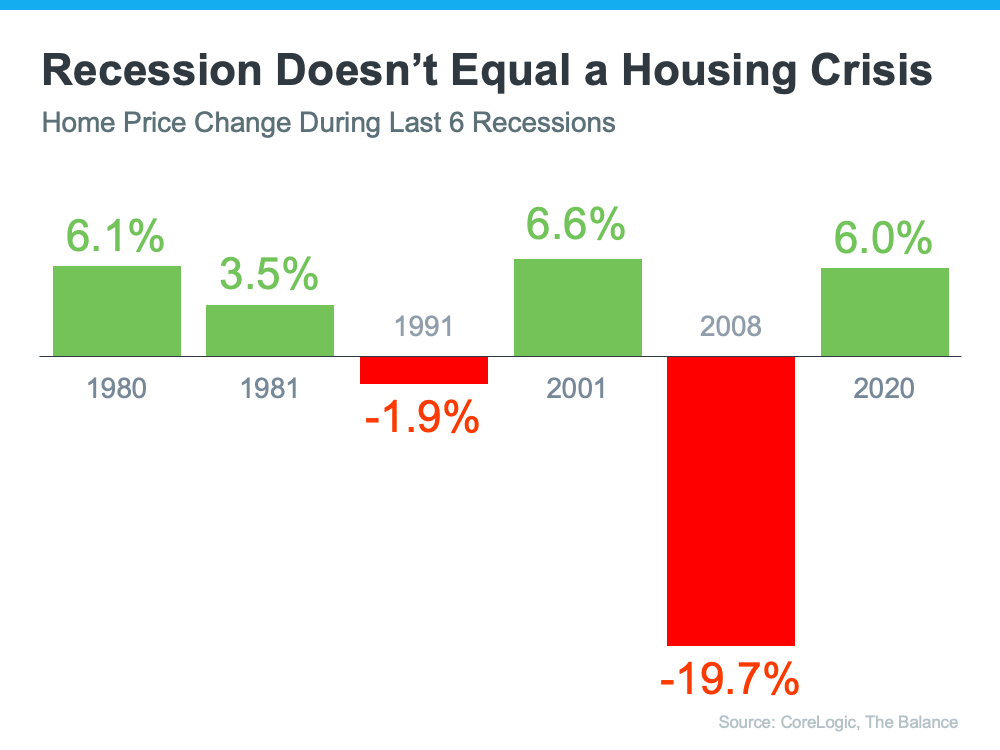

A recession does not equal a housing crisis. That’s the one thing that every homeowner today needs to know. Everywhere you look, experts are warning we could be heading toward a recession, and if true, an economic slowdown doesn’t mean homes will lose value.

The National Bureau of Economic Research (NBER) defines a recession this way:

“A recession is a significant decline in economic activity spread across the economy, normally visible in production, employment, and other indicators. A recession begins when the economy reaches a peak of economic activity and ends when the economy reaches its trough. Between trough and peak, the economy is in an expansion.”

To help show that home prices don’t fall every time there’s a recession, take a look at the historical data. There have been six recessions in this country over the past four decades. As the graph below shows, looking at the recessions going all the way back to the 1980s, home prices appreciated four times and depreciated only two times. So, historically, there’s proof that when the economy slows down, it doesn’t mean home values will fall or depreciate.

The first occasion on the graph when home values depreciated was in the early 1990s when home prices dropped by less than 2%. It happened again during the housing crisis in 2008 when home values declined by almost 20%. Most people vividly remember the housing crisis in 2008 and think if we were to fall into a recession that we’d repeat what happened then. But this housing market isn’t a bubble that’s about to burst. The fundamentals are very different today than they were in 2008. So, we shouldn’t assume we’re heading down the same path.

We’re not in a recession in this country, but if one is coming, it doesn’t mean homes will lose value. History proves a recession doesn’t equal a housing crisis.

![]()