Is It Really Better To Rent Than To Own a Home Right Now?

Is It Really Better To Rent Than To Own a Home Right Now?

You may have seen reports in the news recently saying it’s better to rent right now than it is to own your home. But before you let that impact your decisions, you should understand what these claims are based on.

A lot of the time, these reports are assuming things that aren’t realistic for the average household. For example, the methodology behind one of those reports says that renting is the smarter financial option because of the opportunity to invest money elsewhere. It assumes renters take the money they’d spend on costs tied to buying a home and put it in an investment portfolio.

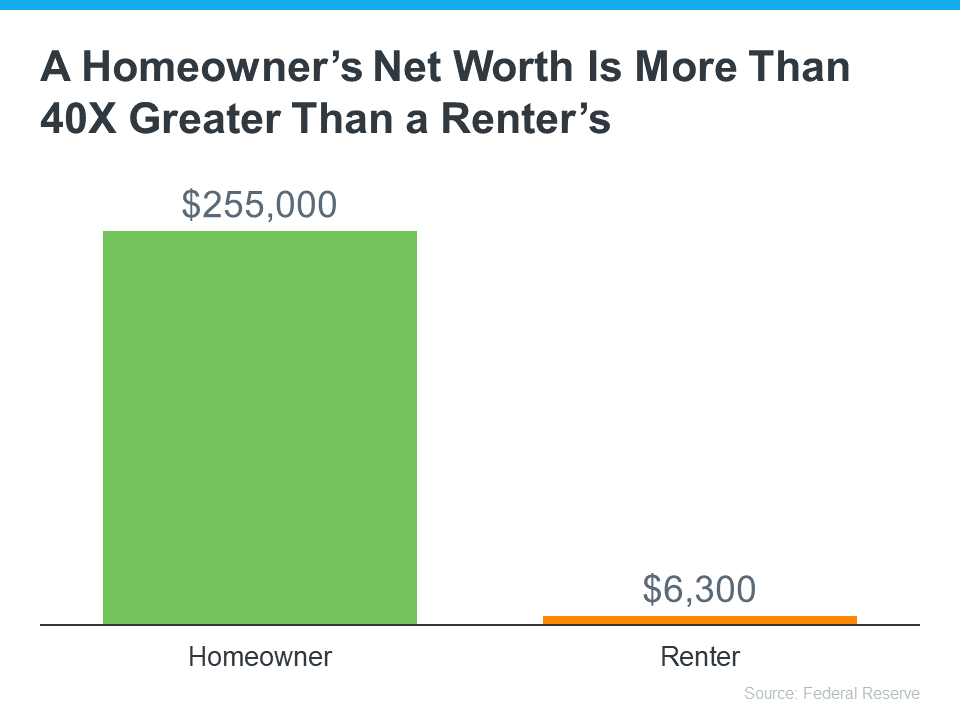

But here’s the thing – most people who rent aren’t making those investments. Ken Johnson, Co-Author of the BH&J National Price-to-Rent Index, explains:

“One of the difficulties with the rent and reinvest model is many people . . . simply rent and spend the difference. . . . That’s wealth destroying.”

The reason homeownership is one of the best investments you can make is the wealth it helps you build. That’s why there’s a significant difference between the net worth of the average homeowner and the average renter (see graph below):

So, before you renew your rental agreement, think about the opportunity to build wealth that homeownership provides.

Bottom Line

If you’re unsure whether to continue renting or to buy a home, let’s connect to help you make the best decision.

Marty Gale

Buy or Sell with Marty Gale

"Its The Experience"

Principal Broker and Owner of Utah Realty™

Licensed Since 1986

CERTIFIED LUXURY HOME MARKETING SPECIALIST (CLHM)

PSA (Pricing Strategy Advisor)

General Contractor 2000 (in-active)

e-pro (advanced digital marketing) 2001

Certified Residential Specialist 2009

Certified Negotiation Expert 2014

Master Certified Negotiation Expert 2014

Certified Probate Specialist Since 2018

Senior Real Estate Specialist

Certified Divorce Specialist CDS

![]()

Contact me!